OCW: Real Yield

Given this is one of the hotter narratives out there in crypto, I thought it would be worth putting together some examples of real vs. unsustainable “yield” or revenues in crypto across some of the major + most shilled projects (and how to research it yourself). Tomorrow I will also be releasing a guide to the merge, while Friday morning I’ll be posting another project deep dive. Side note: if anyone is looking to work with me on anything (advisory, collaboration, sponsorship within the newsletter, etc) feel free to reach out to me at onchainwizard@gmail.com.

#RealYield

Before I dive into some examples, I want to share how you can research this yourself. One of the things I work very hard at with my content is educating crypto investors to improve their independent research capabilities, to hopefully rise up past blindly following twitter or telegram shills for random tokens. This will hopefully be another example of how to do just that.

What does real yield mean in crypto? You are looking for projects that make more than they spend. This is fairly easy to do when analyzing a business or a public company, as you can clearly see their financial statements, and see that revenue is more than expenses. But this is much harder to do in crypto for a few reasons - revenue data can be hard to come by for some projects, if it is not listed on something like Token Terminal. Additionally, revenue for most crypto projects is highly cyclical, and tied to speculation / activity in the crypto space. But lastly (and the key part to look at) is that not all revenue in crypto is created equal. This is because projects will “emit” or give out their token to incentivize usage of their product. This is really an expense from the token holders point of view, because it is (1) a customer acquisition cost, but also (2) it dilutes the value of the token given it adds tokens to the circulating supply base. While at the beginning of a project’s life cycle, it likely does make sense to incentivize usage with token emissions, over time if it wants to retain value, then revenue - token emissions needs to be positive (or else it is just a net negative flywheel).

So how do you research this for yourself? Well first, it is important to note that sometimes “narratives” prove stronger than facts in crypto, so don’t kid yourself into thinking that just because a project trades at a low multiple of revenue without emissions that its token will go up - look at MKR for example, a net profitable business with no emissions, which generated $74mm of revenue in the past year. The MKR token has a ~$1bn market cap / fully diluted valuation. While tokens like DOGE and SHIB (that are just memes) have $9bn and $7bn valuations respectively.

With that said, if you are dealing with less established tokens, the exercise is still worthwhile, as if you spot a true earning protocol before other people catch on, there is certainly money to be made (GMX for example). So how do you go about researching this yourself?

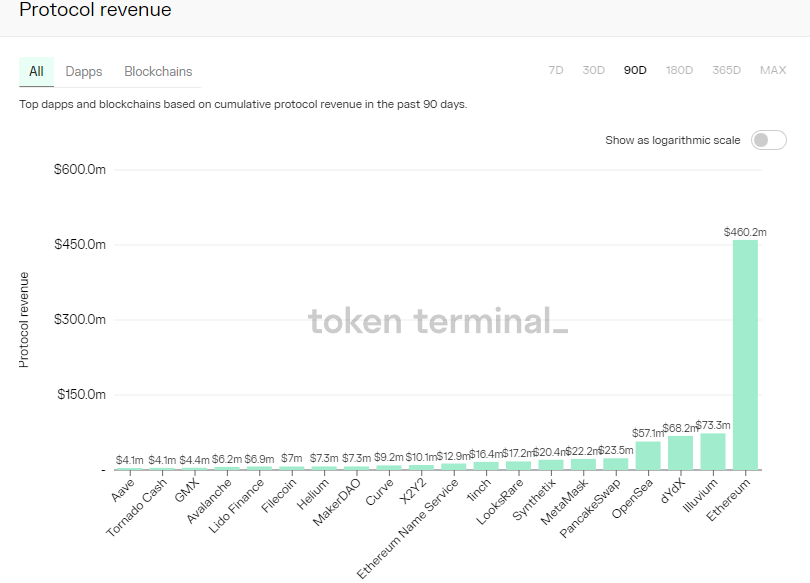

Let’s start with revenue. You can find revenue data for most of the large protocols on Token Terminal, where you can filter by time period. For more off the run projects, if you want to find revenue data, you can look at (1) Dune Analytics to see if there are any dashboards created to track revenue/fee data, (2) some projects will include this data on their website, or (3) you can track it down by jumping into a project’s discord and asking for the wallet where fees are being accrued (especially in examples where fee earning staking have not been launched yet).

This is for historical revenue data, but you can also model out what you think projected revenue could look like using documentation + discord commentary from a project. For example, for DEXs and perp protocols, usually you can apply a certain fee percentage across all trading volume to get a fairly accurate view of what fees/revenue looks like at various levels of activity.

On the emissions side, its more of an uphill battle. For more established protocols, I usually will look at Messari, which has good data on supply side schedules for tokens (below you can see where to find it on their website, which is free to use for this function).

If the data is in Messari, you can look at the supply schedule, and look for any token emission that is incentive / activity based, and this will give you a sense of the emissions for the token (you are not trying to include team + investor unlocks in here).

Using an example, we can look at DYDX (which is being heavily shilled as a “real yield” protocol), to see if the narrative lines up with the data. Looking at TokenTerminal, DYDX revenue over the last 90 days is $68.2mm. Now if we spin over to the Messari emission data, and total what looks like incentive based emissions (trading rewards, mining rewards, LP rewards, staking rewards), we can see that 90 days ago the total circulating supply of the sum of these tokens was ~115mm. Today it is 149mm. So that is roughly 34mm of emitted tokens over this time period, the majority of which were trading rewards (ie incentives to trade on DYDX). At current prices, this is ~$78mm of token emissions / dilution vs. $68mm of revenue = not real yield - and please note I am assuming that DYDX fees would be distributed to DYDX token holders (as they are not currently). While relatively simple to do, most people will not take the few minutes to do their own research, and will respect the twitter shills of this as a real yield protocol as gospel. Again, for sake of simplicity, you can think of real yield as revenue/fees less incentive based token emissions.

Ok, what if a project you are researching does not have token supply data on Messari? You can start with supply schedules in a project’s tokenomics documentation, and again filter for incentive based token rewards and compare them to revenue being generated by the project / protocol. If that doesn’t exist, the last resort can be pulling data from something like CoinGecko to get historical token supply on a project, and then look at the amount of raw token inflation over a time period vs. revenue (this is more crude, as it can include team + investor unlocks).

Now that I’ve given you a taste of how to do it yourself, I’ll walk through some examples of real (and not so real) yield. One more important point though - just because something is not currently generating a positive spread vs. token emissions doesn’t mean its a bad idea. And even more profit can be made in spotting areas where this spread is about to inflect (markets are forward looking, and respond well to incremental changes).

SNX:

As you can see above, 90d revenues for the project were ~$20.4mm. Compare this to token inflation (per Messari) from what is basically just staking rewards, the project emitted 2.3mm of tokens over the same period, which at current prices (you can blend these prices over time if you want) equals $8.8m of emissions. $20.4 - 8.8 = ~$12mm net, which is a very good sign. While there may be team related expenses that get pulled out as well, the overarching point is that the project is making money without being overly dilutive, signaling that it probably is much more sustainable that tokens that are generating highly incentivized revenue.

MKR:

$7.3mm of trailing 90d revenue vs. zero emissions. Very good from a “real yield” perspective.

GMX:

The project generated $4.4mm of revenue over the last 90 days, and if you haven’t been following, does not offer any “incentives” to use its trading platform. So both the yield paid to GMX or GLP stakers (excluding esGMX rewards) are true, sustainable yields.

UMAMI:

This is an Abritrum project, that uses a delta neutral strategy to collect yield from GLP (and hedges it via Tracer). Zero token incentives (that I am aware of), and currently has $4mm in its USDC vault (which is currently capped at $4m). Clear to see that this is also a very real yield (subject to smart contract and hedging risks of course).

LDO:

I’ve seen this one included in some real yield conversations, but a look beneath the surface would show that its not there yet. Lido generated $2.2mm in revenue in the last 30 days vs. roughly 4mm in token emissions (at current prices worth $9m). Now this may change going forward, but not “real” yield yet.

Closing Thoughts:

There are some key points to takeaway from this simple thought + data exercise. First, you should be doing your own independent research to see if the data matches the narrative. But even more broadly, you should be able to quickly see for most protocol products if it is being used organically (without incentives) or not. This is also why TVL is a flawed metric in crypto, as 100s of millions of dollars will flock to chase yield wherever it can get it, but will leave if the yield dries up. Another useful lens to view product revenue / usage through is: will people use this product if there were no incentives, and if the project’s token collapses in value.

The final point I want to drive home is that the examples above are backward looking, and if you really want to have a strong investment setup, you are looking for incrementally positive changes to emissions + revenue. And if you see a product getting a lot of organic usage, there is something special likely going on. For example, one of the ideas I will be writing about this Friday has brought down their token emissions substantially, and has been getting completely organic revenue on their core products. If a token has this going on, while its “narrative” or price are stuck in the past, it could be a advantageous set up (going from bad, dilutive token, to sustainable token). As always, feel free to drop comments or questions below.

Disclaimer: This content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice.

Nice one, thanks sir! Could you please dive into new BTRFLY?

great post, this the helpful stuff for me